“Save early and often.” No doubt you’ve heard this before. And for a good reason.

When planning for a significant expense like college, saving early and often has benefits. Many of us recognize the importance of saving. However, how much to save for college — and how to arrive at the number — is less discussed.

When saving for college, there is no magic number. In fact, most families don’t save for the full cost of college, and because of grants and scholarships, most don’t need to. How much you save will depend on your financial priorities and projected future college expenses, which may be offset by grants and scholarships from the college or university. But there are some steps we can follow to help find our college savings number.

We’ll guide you through each step, and whether you’re looking for a rough estimate or more personalized results, you can choose your own path.

Let’s get started.

1. Research current college costs

The first step in finding your college savings number is researching current costs. Every college and university has a published price, sometimes referred to as the sticker price or cost of attendance (COA). This typically includes tuition and fees, room and board, and supplies. These costs may vary based on where you live (like in state vs. out of state), college residency plans (living at home vs. living on campus), and other factors.

Just starting your savings journey? Research costs at a handful of colleges. Even if your child is young and college is years away, this is an excellent first step for establishing a baseline.

Not sure which colleges to pick? Don’t worry, many students don’t know which college they will attend until well into the senior year of high school. Start with 3 to 4 different types of institutions. For example, you could research a higher price private college ($60,000+/year), mid-range private college ($40-50K/year), and lower cost public university (less than $30,000/year). If you have a better idea of where your child might attend college, choose a specific college or two to look up.

Follow our example to find your number. We’re using average costs and average grants and scholarships for all colleges in 2019-2020.1

Getting to your number

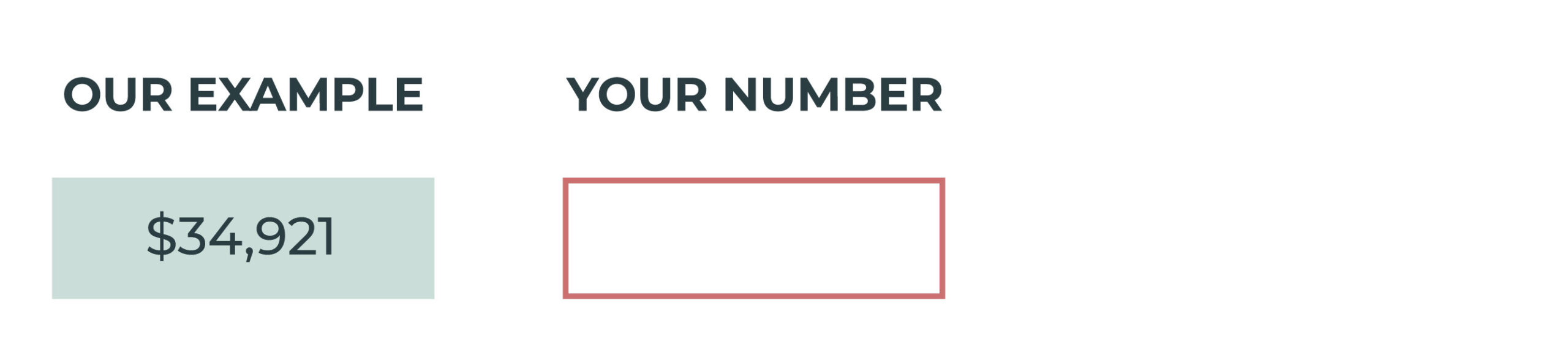

List the institution’s cost of attendance (tuition and fees, room and board, books and supplies).

Rough estimate: Use the average based on college type.1

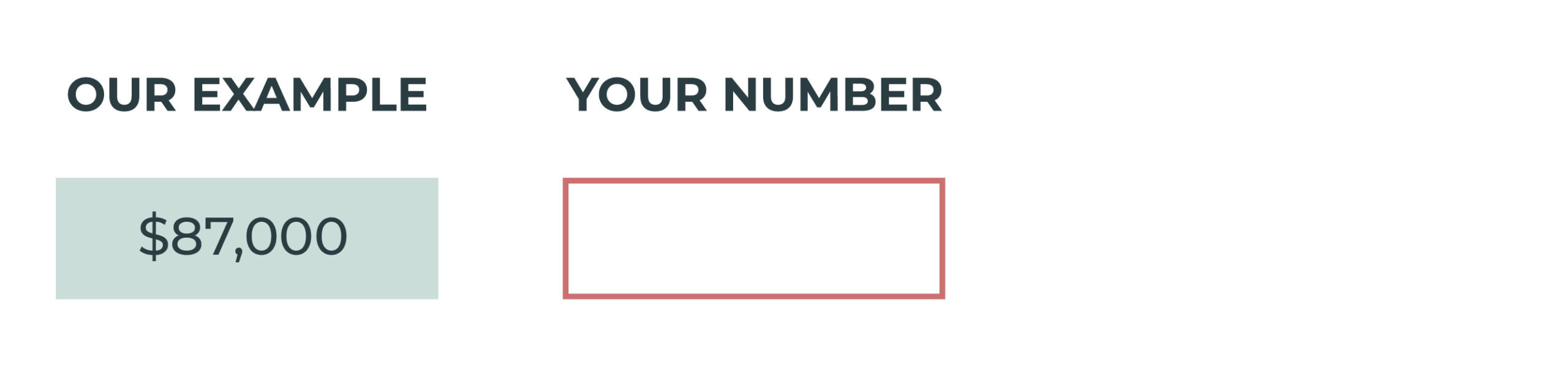

- Average for all colleges: $$34,921

- Average four-year private: $53,376

- Average four-year in-state public: $25,326

Personalized result: Have a specific college in mind? List the cost of attendance for that institution. This can be found on the college’s website or by contacting admissions or financial aid.

2. Factor in projected cost increases

Since colleges determine prices yearly, predicting future increases will be just that, a prediction. However, you can look to historical increases as a starting point.

A helpful site is College Navigator, which provides detailed information on tuition, fees, and estimated student expenses for the past three years at each college across the country. Or you could use an average. According to Education Data, from 2009-10 to 2019-20, private nonprofits increased costs by 4.0% per year on average.

Whatever site or resource you use, go back to that handful of colleges you identified. Or use the average across all colleges, and estimate how much costs will increase over the next 5, 10 or 15 years.

Again, even if your child is young, and you have 10 (or more) years of saving, you can use the average increase of the past few years to project future costs no matter how far away.

Getting to your number

For our example, we’re using a college cost calculator to find the cost when your child enrolls in college, with the following assumptions:

- 10 years until college

- 4 years in college

- 4% rate of annual increase

- $34,921 current annual cost

Don’t be frightened by this number! Again, most families do not pay full price, something we will explore next.

3. Calculate your real cost of college

Once you’ve identified current costs, the next step is determining your actual cost or net price.

One of our experts, Kathy Anderson, explains the difference between a college’s published price (or sticker price) vs. the net price (or your real cost of college).

“You’ll see a published price, a cost of attendance, which is a comprehensive figure,” says Kathy. “It includes tuition and all the other things it takes to be a student, like room and board, books, etc. Then there’s what’s called the net price, which is the price the family will pay after funding from the college itself — grants or scholarships [aka discounting] — is applied toward the cost of tuition.”

Learn more about Your Real Cost of College from Kathy.

How do you determine your net price?

One helpful tool is the College Scorecard, which aggregates information from colleges and universities, including the average annual costs for students after factoring in financial aid (grants and scholarships). You can use the College Scorecard to get an idea of costs at all colleges and universities in the U.S. including the average net price.

Suppose you have a better idea of which college the student may attend. In that case, you could use their net price calculator. This tool estimates what a student may receive in financial aid from the college or university. Every college and university must have a net price calculator on their website. This tool is valuable for anyone. But because it relies on historical data about college financial aid packaging (which changes every year), it will be more accurate if your child is closer to college.

Getting to your number

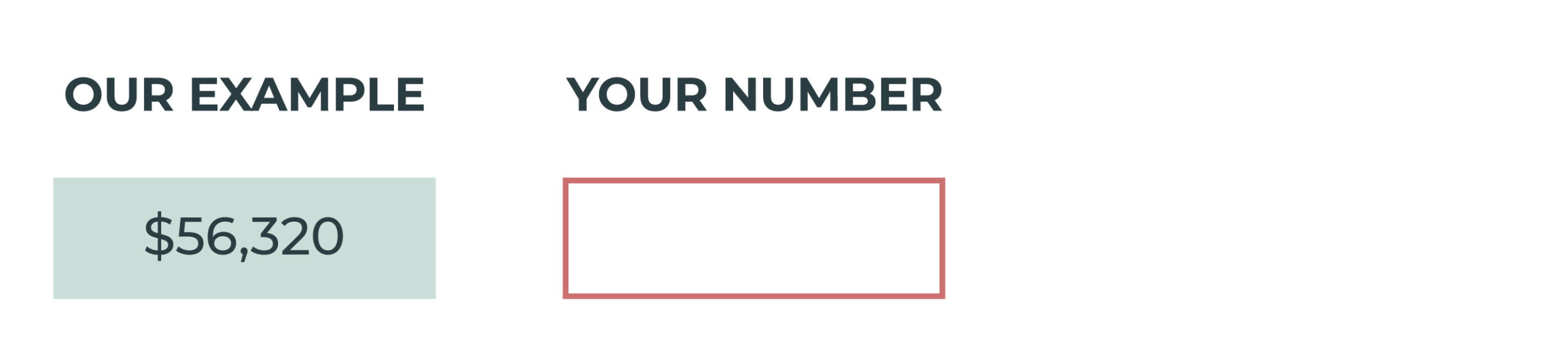

Step 3 (a): Find your potential eligibility for grants and scholarships.

Rough estimate: Use the average based on school type. Multiply that by the number of years the student plans to be enrolled. (In our example, 4 years using the average for all colleges)2

- Average for all colleges: $14,080

- Average four-year private: $25,200

- Average four-year in-state public: $8,600

Personalized result: Use the net price calculator for your selected institution to estimate eligibility for grants and scholarships. Multiply your potential eligibility by the number of years the student plans to be enrolled.

Step 3 (b): Subtract potential grants and scholarships from the cost of attendance (reference step 2) for your potential 4-year net price.

4. Set your target savings goal

Now it’s time to set your target college savings goal. To reach that number, you’ll need to use information from the previous three steps. At this point, you may also want to consider the following to get a more accurate number:

- Family support. Will your student receive any financial support from family? That will help reduce your final number.

- Payments plans. Many families set up a payment plan once their child is in college. Plans are usually offered directly from the college or university and help reduce the amount you need to save ahead of time or borrow.

- Student borrowing (loans). Do you or your student plan on borrowing to cover some college costs? This will further reduce that savings number.

Let’s revisit our example.

Getting to your number

Factor in any additional financial support the student may receive. For each step below, include the total amount for all years the student plans to be enrolled.

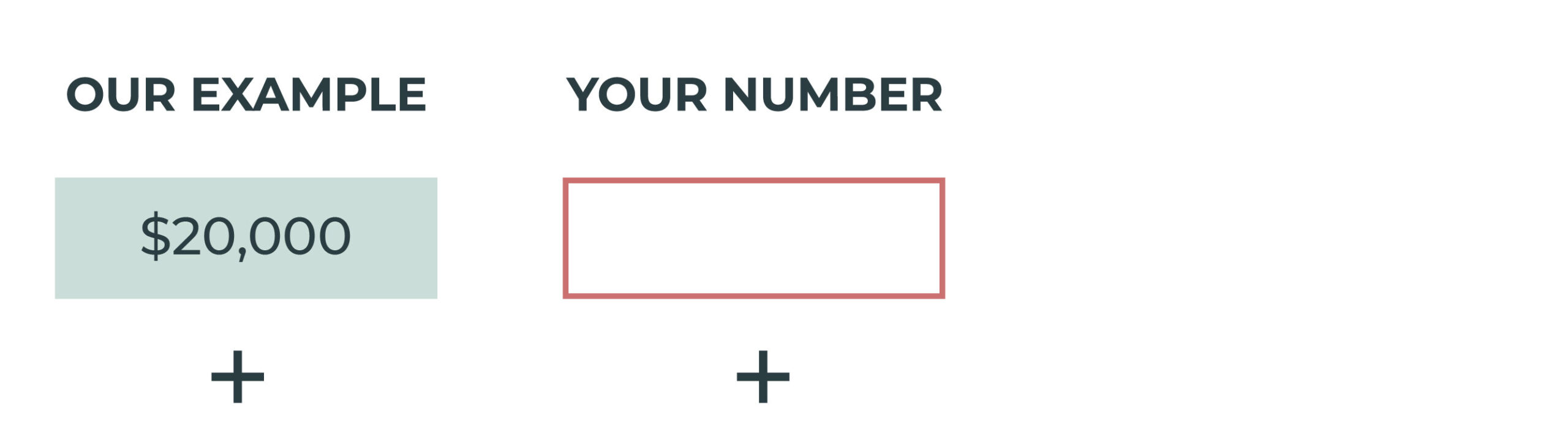

Step 4 (a): List any outside support your student will receive, like from family members or student earnings.

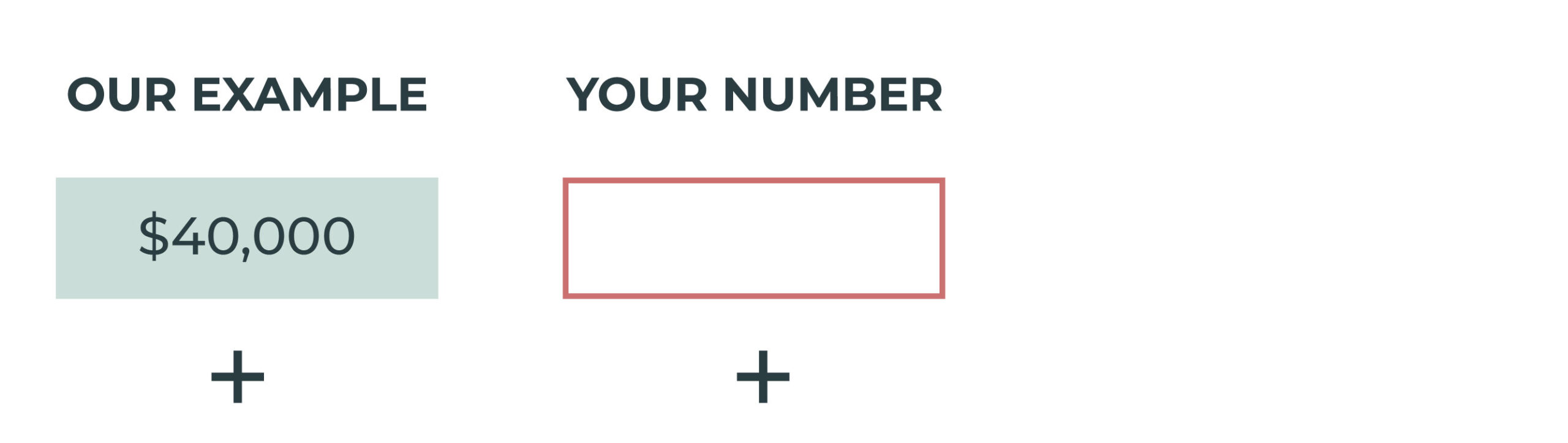

Step 4 (b): Include any payments you plan to make while the student is in college. For example, $1,000 per month in a 10-month tuition payment plan equals $40,000 for 4 years of college.

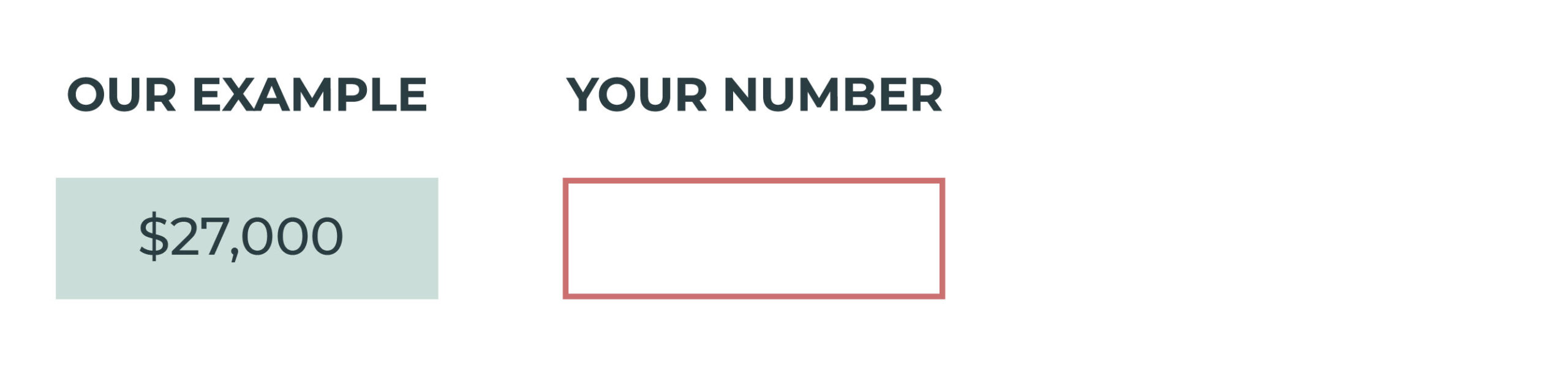

Step 4 (c): If the student will borrow to help cover costs, add that amount here. Currently, if a dependent undergraduate student borrowed the annual limit for 4 years, it would be $27,000.

Step 4 (d) Combine all additional resources.

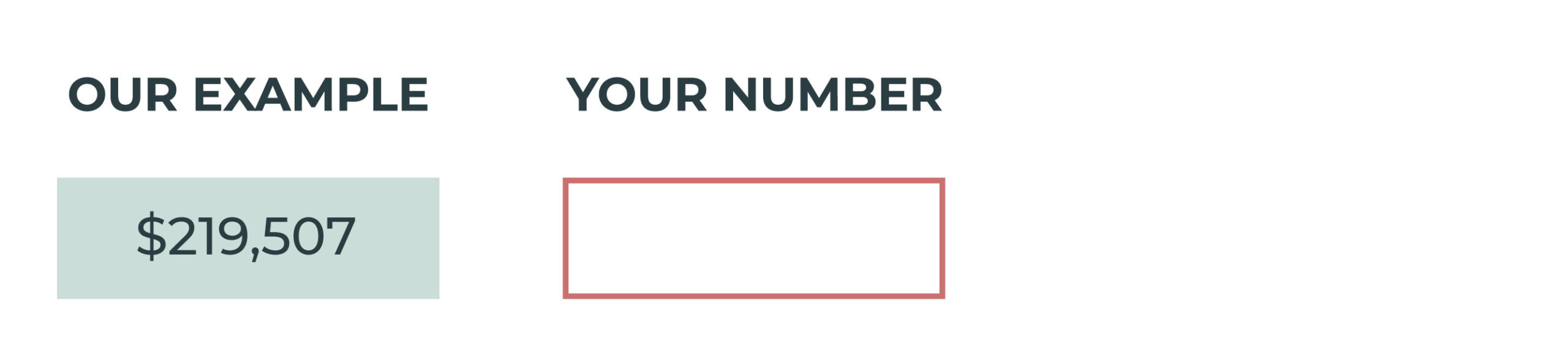

Step 4 (e) Subtract this total from your net price (reference 3b). This is the amount you will need to cover for the total number of years the student will be enrolled.

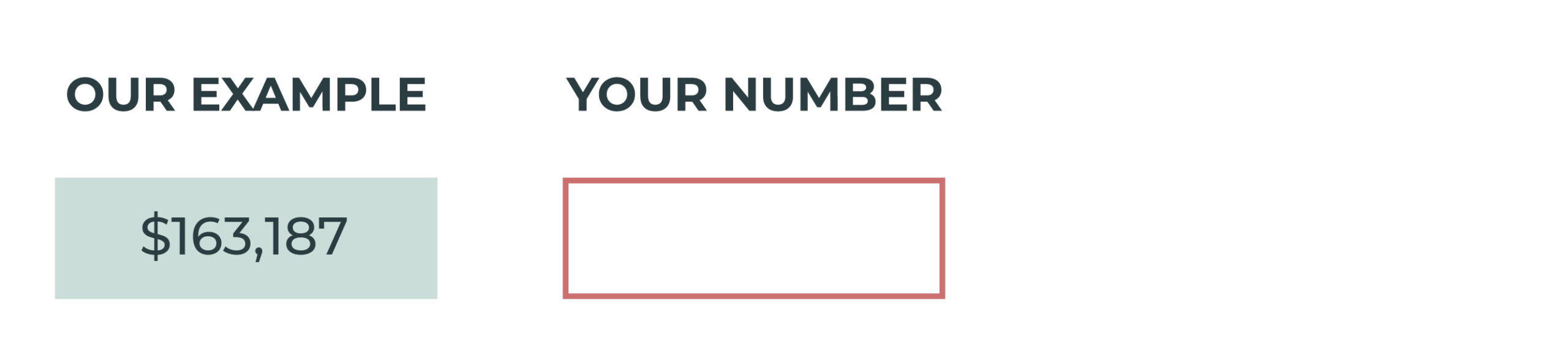

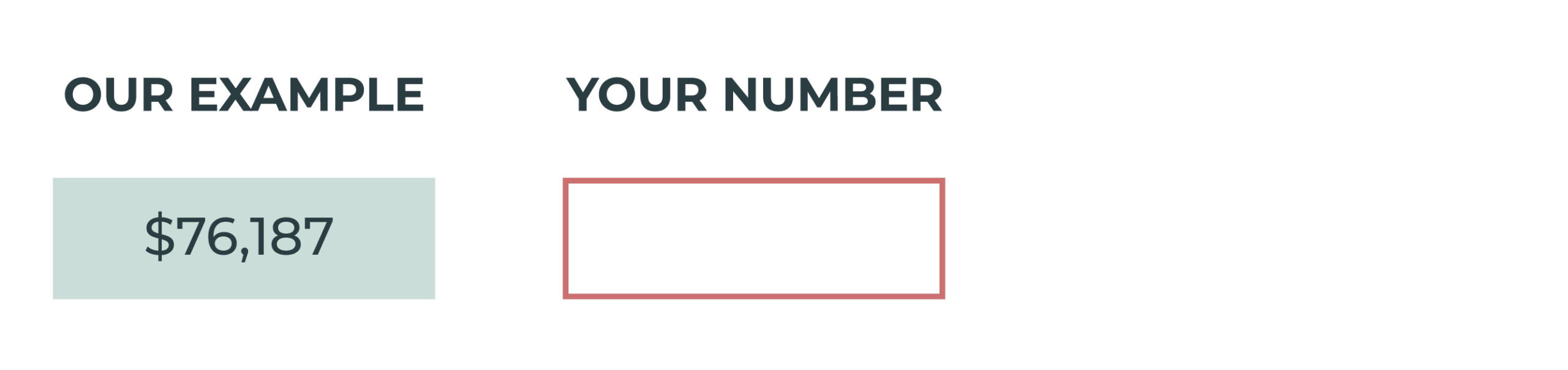

In our example, given all assumptions, the total projected net price for four years is $76,187 — and this is our college savings number.

How are we looking?

If this doesn’t seem like your number, perhaps you only planned to save for two years of college, bringing your number to $38,093, or one year, which would further reduce your number to $19,047. Either way, you have a starting point.

After you land on your number, you next need to think about how you will reach that number. It may be wise to seek out the help of a financial planner or advisor. Consider the following:

- How much to save each month (after factoring in projected returns)

- Does my number match what I can realistically save each month?

- Do I have multiple children planning to attend college? If yes, how will that impact my ability to save?

- How much of a priority is saving for college?

- What financial tradeoffs am I willing to make to save more?

- Options for investing your college savings (529 savings plans, 529 prepaid plans, etc.)

5. Start (or continue) saving

You’ve got your number; now it’s time to start saving. There are many ways to save for college, but a popular – and cost-effective – option is a 529 plan.

529 plans come in two types: savings and prepaid plans. The most popular option is a 529 college savings plan. Anyone can open a 529 college savings plan. Contributions are after-tax, but funds grow tax-deferred, and withdrawals are tax-free when used to pay for qualified higher education expenses.* They’re called savings plans, but many 529s are structured like investment accounts. Meaning you are required to choose an investment option offered by the plan.

Another option is a 529 prepaid plan.

As the name suggests, prepaid tuition plans allow you to prepay all or part of the participating colleges’ tuition and mandatory fees. Like 529 college savings plans, contributions are after-tax, but the increase in value grows tax-deferred. And withdrawals are tax-free when used to pay for qualified higher education expenses.* Many of these plans have a state residency requirement to participate.

An option for private college

If you’re considering private college, there’s a plan designed to help.

Private College 529 Plan is a prepaid tuition plan specifically created to help families save on the cost of tuition at private colleges and universities across the country. It’s the only plan owned by colleges, so there’s no residency requirement to save. As yearly tuition rates increase, the value of your prepaid tuition also goes up. And the best part? You don’t need to worry about your investment. No matter how markets perform or how much tuition increases each year, your prepaid tuition is guaranteed by the nearly 300 colleges in the plan. Check out how prepaid tuition could help you reach your number.

And you can always use both plans. They work great together. Savings plans take advantage of market returns, while prepaid plans help safeguard against volatile markets.

Getting to your number

Enter either the total projected net price for all years the student plans to be enrolled or the number you’ve determined works for your family.

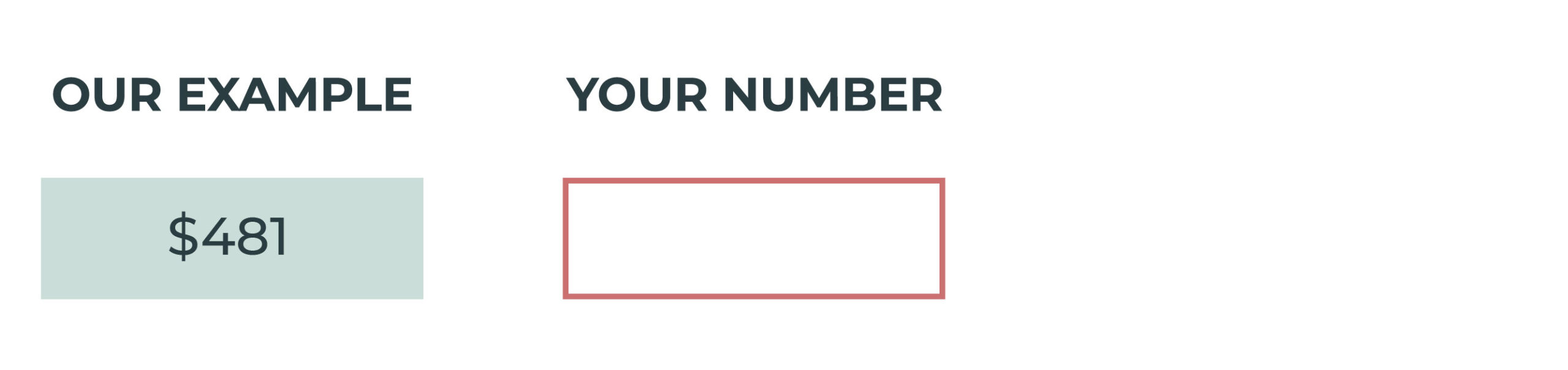

Monthly savings contribution: Use a savings calculator to find your monthly contribution based on this number.3 For example, a monthly contribution of $481 with an initial contribution of $25 growing at 6% interest see will reach $76,187 in 10 years.

Of course, the younger your child, the more of a prediction this will be. A lot can change over 10, 12 or 15 years, so be mindful of this when you use these tools. And make sure to check in on your college savings goal every year.

Notes

*Earnings in 529 plans are not subject to federal tax and, in most cases, not subject to state tax if withdrawals are used for eligible college expenses, such as tuition and room and board. However, if you withdraw money from a 529 plan and do not use it for an eligible college expense, it will generally be subject to a 10% federal tax penalty on earnings in the account. For Roth IRA withdrawals, account owners pay income tax on the earnings portion of investments when funds are used for qualified higher education expenses.

Sources

1. NCES: https://nces.ed.gov/programs/digest/d21/tables/dt21_330.40.asp

2. NCES: https://nces.ed.gov/programs/digest/d21/tables/dt21_331.30.asp

3. Investor.gov: https://www.investor.gov/financial-tools-calculators/calculators/savings-goal-calculator